Almost everyone assumes their cherished belongings are safe once tucked away in a storage unit or spare room. Yet, over 40 percent of college students use off-site storage during school moves and most homeowners do not realize that their standard policies barely cover stored items at all. What may surprise you is that a single event like a burst pipe or a quick theft can wipe out thousands in value overnight and leave you stuck with the loss. The truth is, getting the right insurance for stored items in 2025 could be the easiest way to protect your wallet and peace of mind, no matter if you’re a student, homeowner, or small business.

Table of Contents

Quick Summary

| Takeaway | Explanation |

| Assess Your Storage Needs First | Evaluate the value, duration, and location of stored items before choosing insurance. |

| Understand Coverage Types | Know the differences between replacement cost and actual cash value for comprehensive protection. |

| Document Items Thoroughly | Maintain detailed inventories, photographs, and receipts to simplify claims and prove ownership. |

| Report Claims Promptly | Immediately contact your insurer after damage to avoid delays in the claims process. |

| Compare Multiple Insurance Options | Analyze different plans to identify the best coverage and cost for your specific needs. |

Who Needs Insurance for Stored Items?

Protecting your stored belongings isn’t just for the cautious few. Many people and businesses face unique scenarios where insurance for stored items becomes critical for financial security and peace of mind.

Homeowners in Transition

Homeowners experiencing significant life changes often need specialized storage insurance. Whether you’re renovating your home, recovering from storm damage, or preparing for a major move, your personal belongings remain vulnerable during transitions. Learn more about our storage protection options to safeguard your investments.

According to Insurance Information Institute, standard homeowners insurance typically provides limited coverage for items stored off-site. This means those antique furniture pieces, family heirlooms, or expensive electronics could be at significant financial risk without additional protection.

College Students and Young Professionals

College students and young professionals represent another critical group needing insurance for stored items. With frequent relocations, temporary housing situations, and limited personal storage space, these individuals often rely on external storage solutions. National Student Moving Survey reveals that over 40% of college students use external storage during academic transitions.

Unique challenges for this demographic include protecting electronics, textbooks, clothing, and personal research materials. A comprehensive storage insurance plan can provide financial protection against theft, water damage, or unexpected natural disasters.

Small Businesses and Inventory Management

Small businesses, particularly those in retail, construction, and service industries, critically need insurance for stored items. Inventory represents a substantial financial investment that requires comprehensive protection. Small Business Administration recommends businesses maintain detailed inventories and appropriate insurance coverage for stored assets.

From seasonal equipment to excess inventory, businesses face unique storage challenges. A robust insurance plan can cover potential losses from unexpected events like fires, flooding, or theft. This protection ensures business continuity and minimizes financial disruption during challenging times.

Whether you’re a homeowner, student, or business owner, understanding your storage insurance needs is crucial. Each group faces distinct risks that require tailored protection strategies. By investing in comprehensive insurance for stored items, you’re not just protecting physical objects but securing your financial future and maintaining peace of mind during life’s unpredictable transitions.

What Does Insurance for Stored Items Cover?

Understanding the scope of insurance for stored items is crucial for protecting your valuable possessions. Coverage can vary widely, but most policies share common protections that safeguard your belongings from unexpected risks.

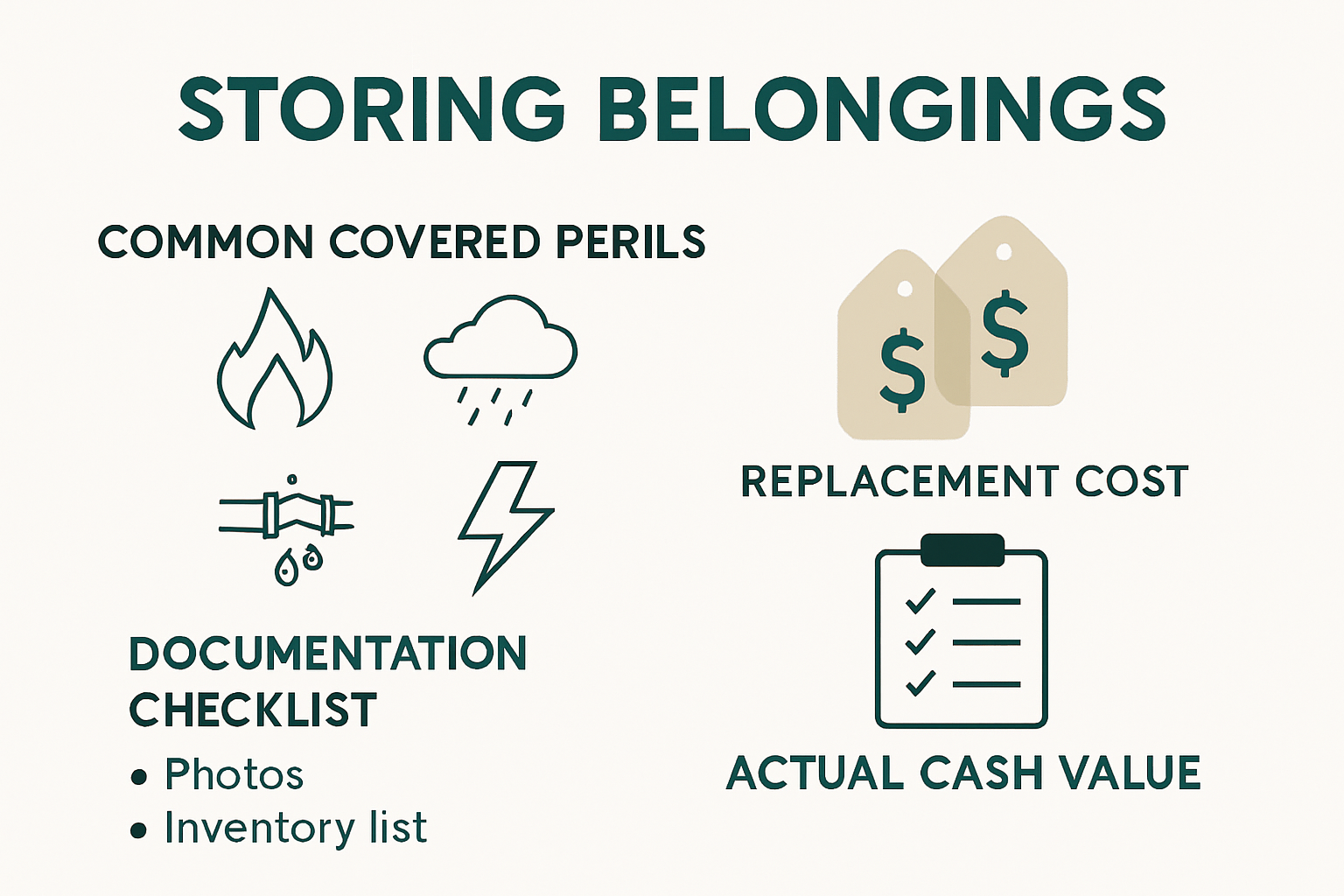

Types of Perils Covered

Insurance for stored items typically protects against a range of potential threats. Learn more about comprehensive storage protection to understand the full extent of potential coverage. According to National Association of Insurance Commissioners, standard storage insurance generally covers:

-

Fire and Smoke Damage: Comprehensive protection against fire-related losses

-

Water Damage: Coverage for flooding, leaks, and water-related incidents

-

Theft and Vandalism: Financial protection against criminal activities

-

Natural Disasters: Protection from storms, hurricanes, and other extreme weather events

It’s important to note that not all policies are created equal. The Insurance Information Institute recommends carefully reviewing policy details to understand specific inclusions and exclusions.

Valuation and Compensation Methods

When it comes to compensation, storage item insurance offers different approaches. Replacement cost coverage provides funds to replace items at current market prices, while actual cash value coverage accounts for depreciation. Consumer Reports suggests that replacement cost coverage offers more comprehensive protection, especially for valuable or hard-to-replace items.

Businesses and individuals should conduct a thorough inventory of stored items. Documenting serial numbers, taking photographs, and maintaining detailed records can significantly simplify the claims process. This preparation ensures accurate valuation and faster compensation in case of loss.

Special Considerations for Different Storage Scenarios

Storage insurance isn’t one-size-fits-all. Different scenarios require tailored protection strategies. Climate-controlled storage might need additional coverage for sensitive items like electronics, artwork, or antiques. Military personnel on deployment, college students storing belongings during breaks, and businesses with seasonal inventory all require unique insurance approaches.

Some policies offer additional benefits like:

-

Temporary Relocation Coverage: Protection during moves

-

Extended Storage Periods: Coverage for long-term storage needs

-

International Storage Protection: Specialized coverage for items stored across borders

While insurance provides critical financial protection, prevention remains key. Proper packing, choosing secure storage facilities, and maintaining regular inspections can significantly reduce the risk of damage or loss. By understanding your coverage and taking proactive steps, you can ensure your stored items remain safe and protected against unforeseen circumstances.

How to Choose the Right Insurance Plan

Selecting the appropriate insurance plan for stored items requires careful consideration and strategic evaluation. Your choice can mean the difference between financial protection and potential significant losses.

Assess Your Specific Storage Needs

Before diving into insurance options, conduct a comprehensive inventory of items you plan to store. Explore our storage protection strategies to understand how to accurately evaluate your belongings. According to Consumer Reports, different storage scenarios demand unique insurance approaches.

Key factors to consider include:

-

Total Value of Stored Items: Calculate the replacement cost of your belongings

-

Storage Duration: Short-term versus long-term storage requirements

-

Storage Location: Indoor, outdoor, climate-controlled, or portable storage units

-

Potential Risk Factors: Local weather patterns, crime rates, and environmental conditions

Compare Coverage Options

Insurance plans vary dramatically in their coverage and cost. The Insurance Information Institute recommends a detailed comparison of available options. Critical aspects to evaluate include:

-

Replacement Cost Coverage: Provides funds to replace items at current market prices

-

Actual Cash Value Coverage: Accounts for depreciation of stored items

-

Deductible Levels: Higher deductibles typically mean lower monthly premiums

-

Additional Peril Protection: Coverage for specific risks like floods or earthquakes

National Association of Insurance Commissioners suggests obtaining quotes from multiple providers to understand the full range of available options. Pay close attention to the fine print and understand exactly what is and isn’t covered.

Understand Policy Limitations and Exclusions

No insurance plan offers unlimited protection. Savvy consumers must carefully review policy limitations and potential exclusions. Some common restrictions include:

-

High-Value Items: Special riders might be required for expensive electronics, artwork, or jewelry

-

Specific Damage Types: Some policies exclude certain types of water damage or gradual deterioration

-

Geographic Restrictions: Coverage might be limited in areas prone to natural disasters

Businesses and individuals should document their stored items meticulously. Take detailed photographs, maintain serial number records, and keep receipts. This documentation can streamline the claims process and provide critical evidence in case of loss.

Choosing the right insurance for stored items isn’t just about finding the cheapest option. It’s about comprehensive protection tailored to your unique needs. By carefully assessing your requirements, comparing multiple options, and understanding policy details, you can secure robust protection for your valuable belongings.

Remember that insurance is an investment in peace of mind. The right plan provides financial security and allows you to store your items with confidence, knowing you’re protected against unexpected challenges.

To help you compare the compensation methods referenced above, here’s a table summarizing “Replacement Cost” and “Actual Cash Value” coverage as described in the article:

| Coverage Method | Definition | Payout Calculation | Best For |

| Replacement Cost | Replaces items at current market price | Full cost to buy new equivalent | Valuable, hard-to-replace items |

| Actual Cash Value | Includes depreciation, pays current value of used items | Original cost minus depreciation | Items with lower replacement urgency |

Tips to File a Claim and Avoid Common Mistakes

Filing an insurance claim for stored items can be a complex process that requires careful preparation and strategic documentation. Understanding the nuances of claim filing can significantly impact your chances of successful compensation.

Preparation Before Damage Occurs

Documentation is your strongest ally in the claims process. Discover our comprehensive storage protection strategies to ensure you’re prepared for potential losses. According to Insurance Information Institute, proactive documentation can dramatically simplify the claims process.

Critical pre-damage preparation steps include:

-

Detailed Inventory: Create a comprehensive list of stored items

-

Photographic Evidence: Take clear, dated photographs of each item

-

Serial Number Tracking: Document unique identifiers for valuable possessions

-

Original Receipts: Maintain records of purchase prices and dates

Here’s a table summarizing the preparation steps to take before damage occurs, making it easier to remember the proactive measures advised:

| Preparation Step | Description |

| Inventory List | Document all stored items in detail |

| Photographic Evidence | Take clear, dated photos of each item |

| Serial Number Tracking | Record unique identifiers for valuables |

| Maintain Receipts | Keep purchase records and dates |

Navigating the Claims Process

When damage occurs, your immediate actions can significantly impact your claim’s success. National Association of Insurance Commissioners recommends a systematic approach to filing claims:

-

Immediate Notification: Contact your insurance provider immediately after discovering damage

-

Prevent Further Damage: Take reasonable steps to protect remaining items

-

Detailed Documentation: Photograph damage extensively

-

Avoid Discarding Evidence: Preserve damaged items until the claims adjuster reviews them

Common Mistakes to Avoid

Insurance claims can be derailed by seemingly minor errors. Consumer Reports highlights several critical pitfalls to avoid:

-

Delayed Reporting: Most policies have strict timelines for claim submission

-

Incomplete Documentation: Insufficient evidence can result in claim denial

-

Undervaluing Items: Failing to accurately assess the full replacement cost

-

Emotional Decision-Making: Avoid hasty or emotional responses during the claims process

Businesses and individuals should approach claims with a methodical mindset. Keep detailed records of all communications with the insurance provider, including dates, names, and conversation summaries. This documentation can prove invaluable if disputes arise.

Timing is crucial in the claims process. Most insurance policies require prompt reporting of damage or loss. Waiting too long can result in claim denial, leaving you financially vulnerable. Create a clear action plan before storing items, ensuring you understand your policy’s specific requirements and time constraints.

Remember that insurance claims are a collaborative process. Maintain open, honest communication with your insurance provider. Be prepared to provide additional information, answer questions thoroughly, and work cooperatively to resolve your claim.

Ultimately, successful insurance claims for stored items come down to preparation, documentation, and strategic communication. By understanding the process, avoiding common mistakes, and maintaining meticulous records, you can navigate the claims process with confidence and maximize your chances of fair compensation.

Frequently Asked Questions

What types of insurance coverages are available for stored items?

Insurance for stored items typically includes coverage for fire, water damage, theft, and natural disasters. Policies can vary, so it’s essential to review the specific perils covered by each insurance plan.

How should I assess the value of items I plan to store?

To assess the value of your stored items, create a detailed inventory that includes current market prices, photographs, and serial numbers. This documentation will help ensure you select appropriate coverage and simplify the claims process.

What is the difference between replacement cost and actual cash value coverage?

Replacement cost coverage provides funds to replace lost or damaged items at their current market price, while actual cash value coverage considers depreciation, paying the item’s current value instead. Replacement cost is often recommended for valuable items.

What common mistakes should I avoid when filing a claim for stored items?

Common mistakes include delaying the claim submission, providing incomplete documentation, undervaluing items, and making hasty decisions during the claims process. Thorough preparation and timely reporting can improve your chances of successful compensation.

Secure Your Stored Belongings with Local Experts You Can Trust

You have just learned how vital the right insurance is for protecting valuables in storage. But insurance alone is not enough. Many homeowners, students, and businesses in South Carolina worry about break-ins, storm damage, or the hidden risks when storing their possessions. Moving and storage transitions often bring stress and uncertainty over whether your things are truly safe or if you will face costly surprises. Stomo understands these concerns because we are South Carolina born and raised.

When you use Stomo’s portable storage and moving solutions, you get more than just a secure, weather-resistant container. Our family-owned team offers personalized service and flat-rate pricing, so you know exactly what to expect with no hidden fees. We deliver your unit, help you pack and even hang your art for you if needed. Emergency, renovation, and temporary storage challenges become simple with Stomo’s quick response and local knowledge. Request your free quote today at https://stomostorage.com and let us show you why we’re the Best of Charleston in 2025. Protect your belongings the right way and experience the local service difference now.